What if Convertibles Do Not Convert?

Part 5 in a series on ownership

This is part five of a series on ownership for founders. This isn’t a series on how to raise, but how to understand different owner perspectives, including your own.

I wonder if future historians will look back at Safes and say they were a temporary invention. They were introduced at the end of 2013 when interest rates were effectively zero. By 2018, interest rates were climbing and (coincidentally?) a less founder-friendly version was introduced: the post-money Safe.

Chris Arsenault, co-founder and partner at iNovia Capital, shared this story about an unconverted Safe:

I’m assuming Chris was talking about an uncapped Safe by the way.

How many people consider what happens if convertibles, well, don’t convert?

Comparing 4 exit scenarios

I’m going to compare Safes and convertible notes to preferred shares if no further capital is raised.

Imagine a startup that raises $1M, either as a Safe, convertible note or preferred shares. That company never raises again.

I’ve mapped out 4 exit scenarios:

Bankruptcy, where assets are liquidated

A minimal return of $1M, where not everyone is made whole

A good return of $10M

A great return of $100M

Safes

A Safe is treated no better than shareholders in a bankruptcy. It will be a write-off. When there is $1M to return, only V2 (post-money) Safes will get their money back. V1 did not have a liquidation preference.

In either of the good exits an uncapped Safe will just get their money back and a pat on the back. A capped Safe will convert into shares. In our example, $1M / $5M = 20% of the proceeds.

In other words, a cap is equivalent to an investor setting a valuation. People should stop saying Safes defer the valuation discussion.

Convertible Notes

A convertible note is ever so slightly better in a bankruptcy in case there is money leftover after creditors are paid. It’s unlikely, but non-zero. Where there is $1M to distribute convertible notes rank ahead of SAFEs and other shareholders. Plus they are entitled to interest. Again, slightly better than SAFEs.

Notes are about the same as SAFEs in positive exits considering the interest is relatively small.

But convertible notes mature, i.e. they have to be repaid. So they are much better than SAFEs in one way: they force a conversation between investors and founders about what the liquidity plan is for the company. Founders might not like that pressure but a maturity date doesn’t stop investors from being reasonable, even converting into shareholders.

Preferred Shares

Preferred shareholders get nothing in a bankruptcy. They almost always have a 1x liquidation preference so they would be made whole if there was only $1M to distribute. With the bigger exits they would earn the same as either SAFEs or convertible notes.

But being a preferred shareholder has many advantages that are well suited to professional investors like VCs.

Having a board seat and information rights gives investors more insight into this company to evaluate risk and opportunity. Protective provisions like vetos and approvals on large expenditures add additional downside controls. VCs would argue these help the company become successful.

Remember in my example neither side knew the company wasn’t going to raise more capital. That means having pro rata rights to invest would be very valuable. Those exist for Safes only if you use the special side letter. Convertible notes, eg TechStars, have them but others may not.

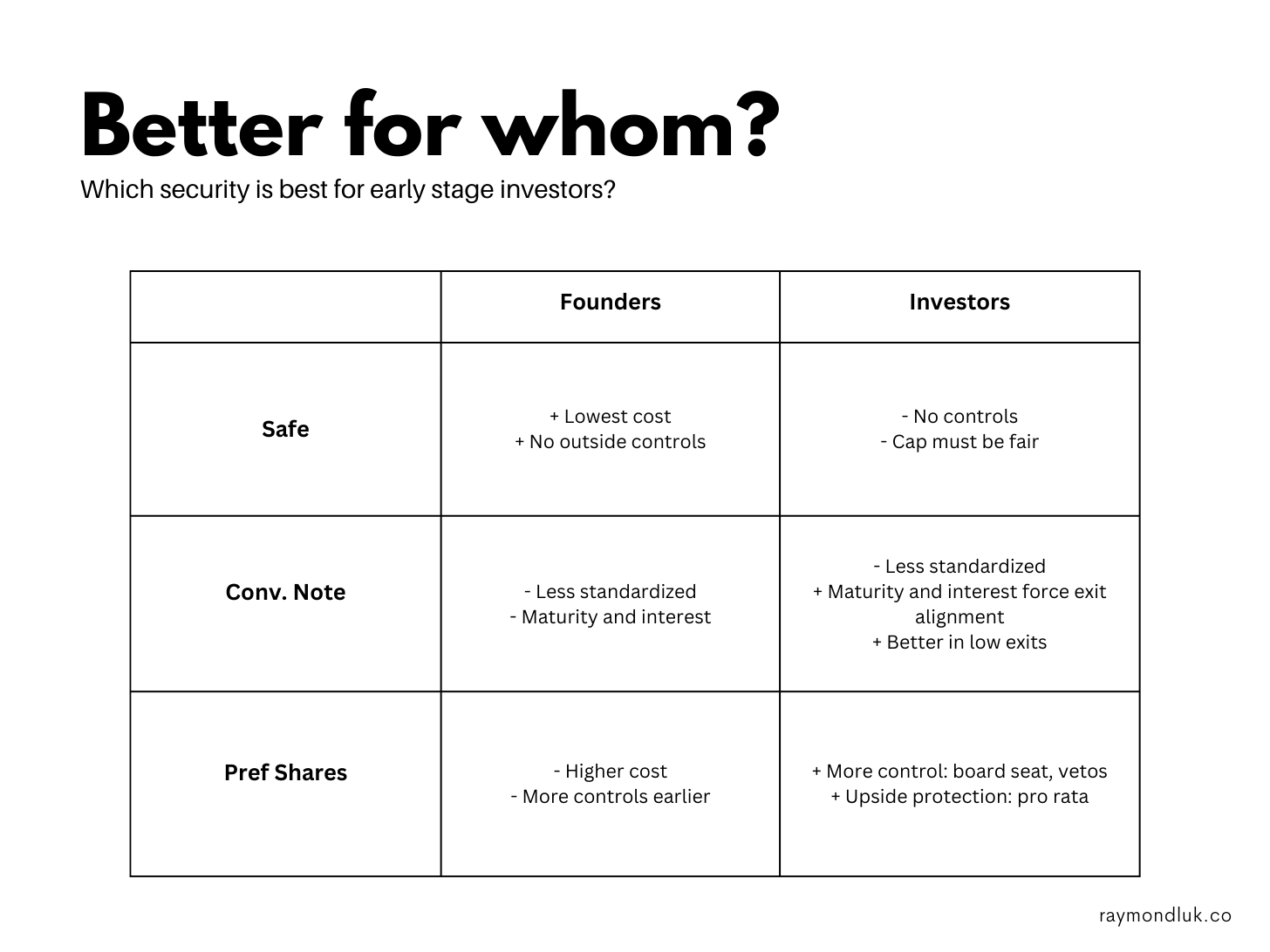

Summary

Taking into account the different exit scenarios and the possibility a company will never raise more money, I’ve created a table comparing the pros and cons of each type of investment:

Three insights:

If the trend continues, and interest rates stay high, Safes could continue to become more like convertible notes. When do downside protections matter the least? When capital is cheap. But capital is expensive now. Who wouldn’t want to be a creditor when things are bad, and shareholder when things are good?

If convertible notes were standardized they would be the ideal early stage investment vehicle. Founders shouldn’t care about giving downside protection and this adds useful incentive to bridge rounds. The upside is exactly the same as Safes.

I’m not sure why any seed fund would use a Safe instead of preferred shares. You are setting a valuation via the cap and the extra controls and shareholder rights are useful. Why not say “I’m all in” instead of “Let’s hope you find other investors.”